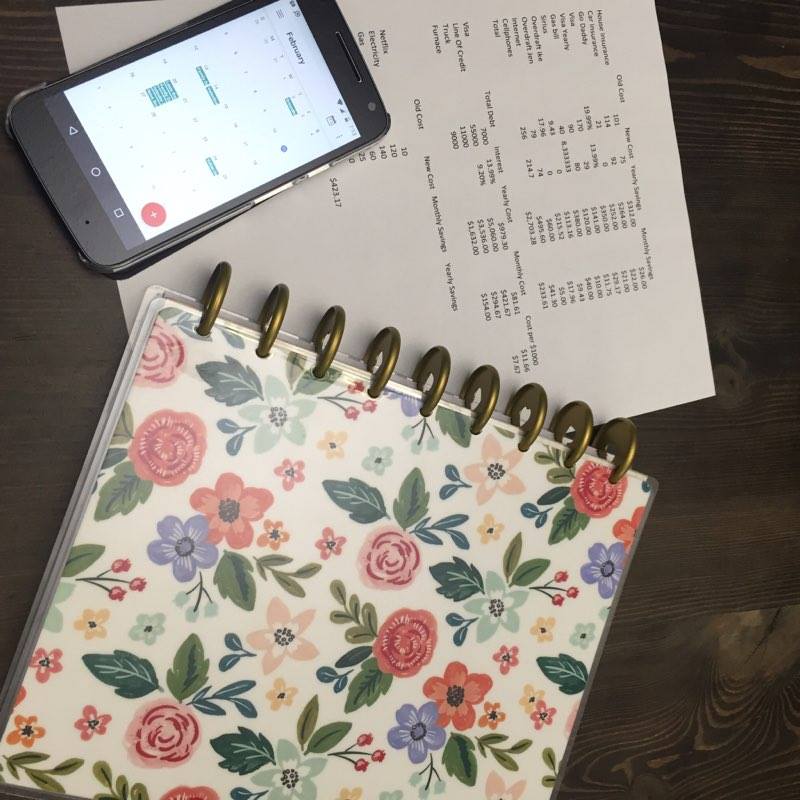

Now that we have looked after the low hanging fruit, what is the plan for our debt? We looked at interest rates, amount and cash flow to determine which to tackle first.

|

In Order

|

Begin Balance

|

Interest

|

Yearly Cost

|

Monthly Cost

|

Cost per $1000

|

|

Visa

|

7000

|

13.99%

|

$979.30

|

$81.61

|

$11.66

|

|

Truck

|

11000

|

$3,536.00

|

$294.67

|

||

|

Furnace

|

9000

|

$1,632.00

|

$154.00

|

||

|

Line of Credit

|

55000

|

9.45%

|

$5,197.50

|

$433.13

|

$7.88

|

We decided to focus on paying down Visa first. It has the lowest balance with the highest interest rate. Having a lower interest rate on this card will help us get this paid down much quicker.

Paying off the truck loan is second for us. Because it is a loan rather than credit, we are not really saving any interest by paying this off. It does however free up $294 per month of cash flow. By looking after this loan we will be able to pay down the rest of our debt quicker.

6 years ago, in the middle of a heat wave, our central AC went kaput!! Of course, we didn’t have money available to cover the replacement. When the salesman came to meet with us we also looked at the furnace. It was also in rough shape so we replaced both on a loan. Over the 10 years of this loan we will pay almost double what the furnace and AC actually cost to replace. A good example of the cost of not planning ahead and having an emergency fund. This one is again a loan, so not saving any interest, just freeing up cash flow to pay down the big one quicker.

Last is the big ol’ line of credit. I still need to call the bank to see if we can lower the interest rate. For every $1.000 paid down, we will save almost $8 so once we get into this we will continue to gain momentum and additional cash flow. I am looking forward to paying this one off the most.

We haven’t outlined goals for when we want to get this done yet. Will post once we figure that out. For now at least we know our strategy and priorities.

We need some goals for February, it is right around the corner.

Thanks for reading, please leave your comments.

Ike & Jen